Part 2: How to Get the Best Mortgage Rate (Plus a Checklist banks will hate)

Whether you’re securing your very first mortgage or staring down a renewal notice, this one’s for you.

In this post, you will learn:

Why the first rate offered by banks is often not the lowest

How to use competing offers to negotiate a better mortgage rate

When a mortgage broker can help you secure a lower rate

How your credit score, income, debt ratio and down payment affect your rate

Simple strategies that can save you thousands of dollars over the life of your mortgage

In Part One, we covered how mortgages actually work. Now comes the part everyone really cares about: how do you secure the best mortgage rate for you.

Most Canadians accept the first mortgage rate their bank offers. That can be a very expensive mistake.

Mortgage rates in Canada are negotiable, and even a small difference in your rate can save tens of thousands of dollars over the life of your mortgage.

A better rate might only take a few emails or phone calls, but the savings can last for decades.

This article applies whether you are buying for the first time or renewing an existing mortgage. Different stage, similar strategy.

Step 1: The Shopping Phase

In Part One, we learned that mortgage rates are largely driven by Canadian bond yields for fixed rates the Bank of Canada policy rate for variable rates. Lenders do not pull numbers out of thin air: rates move with the market conditions.

By following financial news even casually, you can usually tell whether rates are expected to rise or fall in the coming months. This is one of the biggest factors you do not fully control.

The good news is that you can often lock in a rate ahead of time while you shop. If rates go up before you close, you keep your lower rate. If rates go down, you are not stuck: you close at the lower rate. Planning ahead is key.

You can check daily posted mortgage rates on sites like the Financial Post. Think of these as temperature checks, not final answers. Banks also post rates online, but the truth is you can often get even better rates than what is posted - if you shop around and if you qualify.

Shopping around matters, I cannot stress this enough.

Within banks, you will usually deal with a mortgage specialist who can only offer that bank products. A mortgage broker, on the other hand, shops your application across multiple lenders and can sometimes access rates from smaller institutions that do not advertise directly to consumers.

Neither option is wrong: the mistake is not comparing offers. You would not buy a car (or a purse) without comparing prices. A mortgage deserves at least that level of effort.

And you will thank yourself later for it.

Posted rates vs real mortgage rates

Mortgage rates you see advertised are often posted rates, which are essentially starting points. In practice, many borrowers end up paying a discounted rate after negotiation or through a broker.

Banks publish posted rates partly because they are used to calculate mortgage penalties, especially for fixed mortgages. The rate you are actually offered will usually be lower depending on factors such as your credit score, down payment, and the lender you choose.

That’s why it is important to compare multiple offers and ask lenders if the rate is negotiable. Two borrowers with similar profiles can sometimes receive noticeably different rates simply by shopping around.

Step 2: When to start shopping

You might be asking yourself when to start shopping: this will depend on whether or not you are on the market to buy a home, or up for a mortage renewal.

The preapproval

If you are buying, start with a preapproval early. Many sellers and real estate agents will not take you seriously without one. You will need to submit a lot of financial documents to prove income, net worth and credit score.

A preapproval does two important things: it locks in an interest rate for a period of time, and it forces you to run the numbers on how much house you can afford..

Preapprovals can now be done online or with a lender or broker. Most rate holds last around 90 to 120 days depending on the lender.

This is not just theory: this is real life with receipts.

At the end of 2022 I was pregnant and we were officially done with our 800 square foot city apartment. We needed space for a baby. I wanted a walk in closet and a backyard, my husband wanted a man cave with a TV. We all have dreams.

Because rates were expected to rise in 2023, we did the most unsexy adult thing possible and locked in our mortgage rate early with a preapproval, even before we started visiting houses.

Fast forward to winter 2023: we closed on our home using that locked in rate while everyone else was dealing with higher ones (above 5% at the time). Planning ahead saved a lot of money on our mortgage.

If rates drop while you are shopping, you can always request a new preapproval. Locking early does not trap you; it protects you.

Hot Money Mom Tip

Lenders will often approve you for more than you should comfortably borrow. The number you get should be taken with a grain of salt because house poor is not the vibe.

Renewals

Do not sleep on this: if you are renewing, the biggest mistake people make is waiting. Your lender is obligated by law to send you a renewal notice at least 21 days before the end of your term. This notice will contain an offer: it is convenient, lowkey, and designed to be accepted without questions.

You are allowed to say “no”, and shop around. Sorry not sorry.

But here is what most people don’t know: if you go with a new lender, most (but not all) allow you to “hold” in a renewal rate about 90 to 120 days before your term ends (read the fine print and make sure it’s a hold, not a commitment). That is your cue to start shopping. Put a reminder in your phone. Seriously.

You can shop around, negotiate, switch lenders, change terms, or move from variable to fixed. Switching lenders does require a full application, so do not wait until the last minute unless you enjoy stress. (Note: if you stay with your current lender you will not have to submit a new application, meaning credit checks, proof of income, etc. will not be needed).

If you ignore the renewal entirely, your lender may auto renew you into a short term. This buys time, but rarely buys savings.

Also be cautious of promotional renewal offers from you lender that may be went months ahead of time. They may look attractive, but sometimes they are offered because the lender expects rates to fall and wants you locked in.

Step 4: Get your finances ready

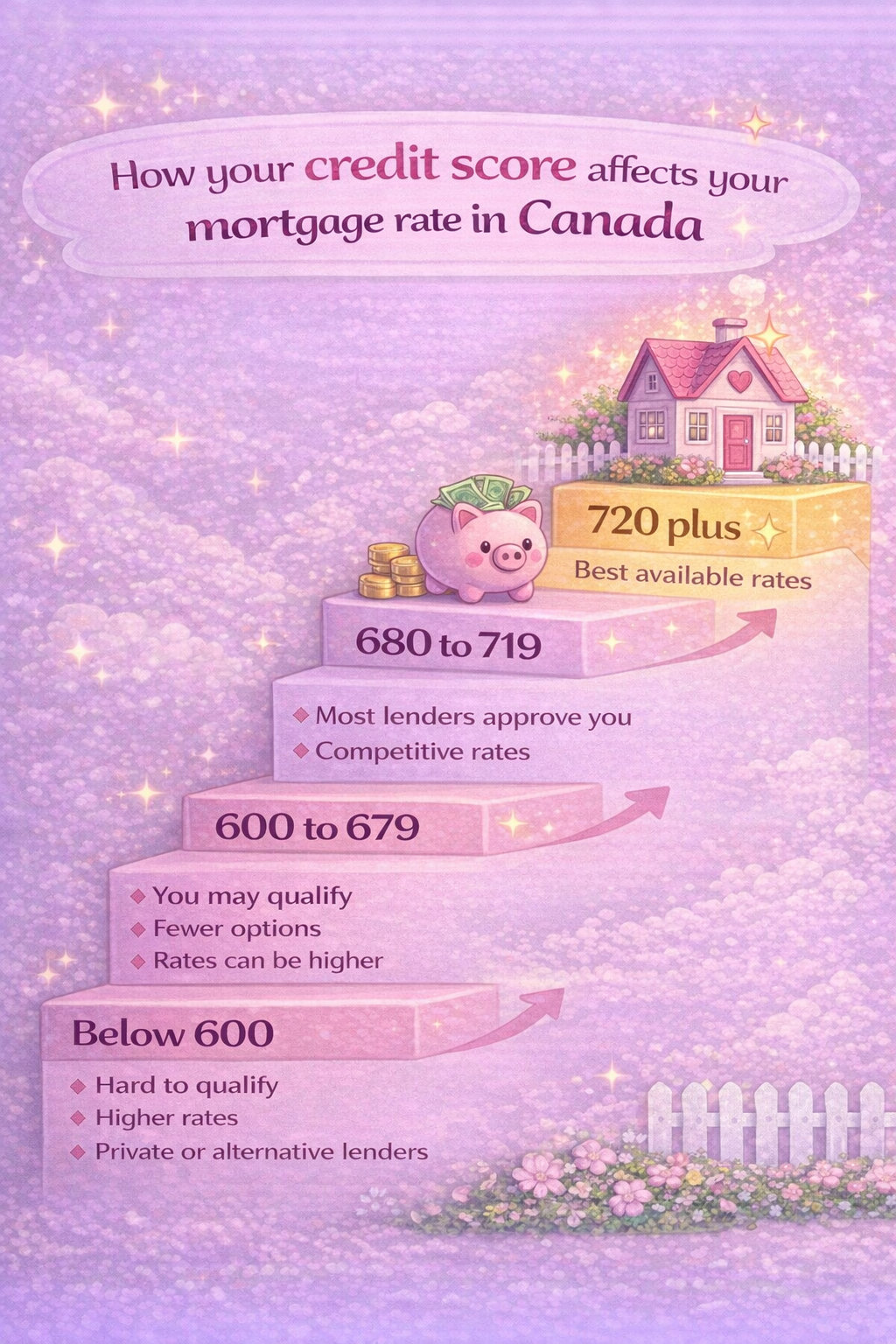

This is not the time for chaos. Before applying or renewing, check your credit score. Ideally, you want it in the good to very good range.

This is not the moment to close credit cards, open new ones, or take on new loans. Stability is your friend.

Credit scores work in tiers. A small jump in score does not dramatically change your rate. But crossing certain thresholds does.

Once you are above roughly 720, you usually access the best rates. Below 680, options narrow. Below 600, rates can increase significantly and alternative lenders may be your only option.

The difference between strong credit and weak credit can mean several percentage points over time. That adds up quickly.

If you are renewing with the same lender, your credit score is not rechecked as you do not need to submit a new application. But if you plan to switch lenders, it absolutely matters, and being able to switch can help you lock in the best rate.

You can find ways to check your credit score on my Resources page. Also, keeping your total monthly debt payments below 44% of your gross income can help. This is called your debt ratio ans shows whether you can actually afford more debt - you might have a good credit score, but a high debt ratio. Lenders will take this into account.

Step 4: Negotiate (because you can)

Mortgage rates you see advertised are often posted rates, which are essentially starting points. In practice, many borrowers end up paying a discounted rate after negotiation or by working with a mortgage broker.

Banks publish posted rates partly because they are used to calculate mortgage penalties, especially for fixed mortgages. But the rate you are offered can often be lower depending on your financial profile and how competitive the lender wants to be.

You might be surprised how often a simple question like “Is this your best rate?” can lead to a better offer (Make sure to download the checklist at the end of this article for other questions worth asking.).

After all, if you don’t ask, you don’t get.

It can also help to bring quotes from other lenders. When lenders know you are comparing offers, they may be willing to sharpen their pencil to earn your business.

Even a small reduction in your interest rate can save thousands of dollars over the life of a mortgage, so it is often worth taking the time to negotiate.

Step 6: Beware of promos and upsells

Banks are often willing to offer a slightly lower mortgage rate if you bring more of your business to them. This practice is called cross-selling, and it simply means the bank earns more from the overall relationship.

For example, you might be offered a better rate if you also keep a chequing account, investments, or other financial products with the same bank. In some cases, banks reserve their most competitive mortgage rates for clients who agree to bundle additional services such as credit cards, insurance, or lines of credit.

Why do they do this? A client who uses multiple products is usually seen as more loyal and less likely to move their mortgage elsewhere, which makes the relationship more valuable to the bank. Sometimes the incentive is not just a lower rate either. Banks may also offer cash bonuses or promotions for bringing your mortgage and other accounts under the same roof, which can help reduce the overall cost of borrowing.

However, it is important to look at the full picture before agreeing to a bundle.

A slightly lower rate is not always worth it if it comes with a $30 monthly chequing account, mortgage life insurance you did not plan to buy, or another credit card you do not really need. Mortgage life insurance offered by lenders can also be more expensive and less flexible than a regular term life insurance policy purchased independently.

Before agreeing to any bundle, ask a simple question:

“If I cancel these products later, will I still keep my mortgage rate?”

Some of the lowest advertised mortgage rates come with conditions attached, so make sure you are looking at the total cost of your mortgage, not just the headline interest rate.

And even when a bank offers a bundled deal, it is still worth comparing offers from other lenders to make sure the full package truly works in your favour, by keeping in mind that some lenders offer competitive mortgage rates without requiring you to open multiple accounts or purchase additional products.

Hot Money Mom truth: A slightly higher rate with flexible terms can be cheaper in the long run.

Step 7: Other things to consider (the fine print that costs money)

When you receive a mortgage offer, do not assume the rate is final.

Always ask : “Is this your best rate?” Lenders often have some flexibility and may be able to reduce the rate slightly to win or keep your business.

When people talk about getting the “best” mortgage rate, they usually mean the lowest number they saw in an ad (or on a community Facebook page). But here’s the hidden truth: the interest rate is only part of the story. The terms attached to that rate can cost you far more than a few decimal points.

One big one is penalties. Fixed rate mortgages often come with much higher penalties if you break the contract early, whether that’s because you move, refinance, or life simply happens. Variable rate mortgages usually have lower, more predictable penalties. A mortgage with a slightly higher rate but flexible penalty terms can end up being cheaper in real life, not spreadsheet life. Read more about penalties here.

Another overlooked detail is prepayment privileges. Some mortgages let you make extra payments or lump sums each year without penalty, others don’t. If you plan to throw bonuses, tax refunds, or side hustle money at your mortgage, this may be important to you. A low rate with no flexibility can slow you down more than you think. You can read about your prepayment rights here.

You should also look at portability. A portable mortgage lets you move your mortgage to a new home without breaking it. If there’s a chance you’ll move before your term ends, this feature can save you thousands. Most people only learn about portability after paying a painful penalty.

Finally, there’s insured versus uninsured mortgages. Counterintuitive but true: mortgages with less than a 20% payment often get lower rates because the lender’s risk is insured (that is right: this insurance protects the lender and not you). That does not mean one option is better than the other, but it’s a good reminder that “bigger down payment equals better rate” is not always automatic.

Hot Money Momreminder: the best mortgage is not always the lowest rate. It’s the one that fits your life, your cash flow, and your exit options. Shop accordingly.

The takeaway

The biggest factor in your mortgage rate will always be timing, bond yields and the Bank of Canada policy rate. Luck plays a role. But there are things you control:

Start early, shop around, protect your credit score & debt ratio.

Choose the right product for you, not just the lowest rate. Did I mention you should shop around ?

Securing the best mortgage rate in Canada usually comes down to three things: having a strong financial profile, comparing offers from multiple lenders, and understanding how banks price mortgages. The lowest advertised rate is not always the best mortgage if it comes with restrictive terms or unnecessary product.

Even a small difference in rate can mean tens of thousands of dollars over time. This is not about being perfect: it is about planning ahead and knowing your got the best mortgage for your needs.

And because I got your back, I prepared a printable checklist with questions you can ask lenders. Your bank or lender just might hate this.

Also check out my Resources page which includes links to mortgage calculators and everything else you need regarding mortages.

Want to learn about more smart strategies like these ? Sign up for my newsletter so you never miss a post.