Everything RESPs: The Money Lesson They Forgot to Teach Us in School

How government grants, investing and time could turn a few hundred dollars a month into over $100,000 for your child’s future.

This guide covers everything you need to know about RESPs, including:

What an RESP is (and why opening one is only step 1)

Family, individual and group RESP plans - including which one to avoid

Whether RESP money can be used abroad

Federal and provincial grants (CESG, QESI, BCTESG & CLB)

How much to contribute to maximize grants

Front loading strategies

How RESP taxation works

Withdrawal rules and limits

What RESP money can be used for

What happens if your child does not go to school

Whether money can be transferred between children

Where to open an RESP

What to invest in inside an RESP

My family’s actual RESP strategy and projections, with real numbers

Grab a coffee: this one is thorough… but future you (and future expensive child) will thank you.

As parents, we want the best for our children. We want them to be happy, healthy, emotionally stable enough not to need 17 Stanley cups, and ideally not drowning in student debt before they have even figured out how to properly separate laundry.

One of the best ways to help with future education costs is by opening a Registered Education Savings Plan, better known as an RESP. This is a registered account that allows you to save for a child’s education after high school. The big magic? The government can add money through grants, and the money inside the account can be invested and grow over time.

For my children, I project that their RESPs could reach over $100,000 each by the time they need the money, for a total of over more than $200,000 for 2 kids. The wild part is that this projection involves contributing roughly $36,000 of our own money per child. The rest would come from government grants and investment growth. Does that sound too good to be true? It is not.

That is the magic of government matching, investing, and compound growth.

Tiny baby today, future expensive adult tomorrow. Did I get your attention ? Keep reading to learn more.

1. First, what is an RESP?

An RESP is a Registered education savings account used to save for post secondary education. That can include university, college, cégep, trade school, vocational programs, and other eligible programs after high school. And, as we will learn below, the money does not have to exclusively used for tuition, but for many expenses relating to education, including books, living expenses, transportation, etc.

But here is the important part: an RESP is not an investment by itself.

The RESP is the account. Inside the account, you still need to decide what to hold. Depending on where you open it, you may be able to invest in ETFs, mutual funds, GICs, cash, stocks, bonds, or other investment products. Opening the RESP is step 1, and investing the money is step 2.

If you open an RESP and leave the money sitting in cash for 18 years, the account does not magically turn into a tuition fairy godmother. The grants help, but investing is what can really help the account grow over time.

2. Who can open an RESP?

Any Canadian resident with a valid SIN number can open an RESP. You can open one for your own child, someone else’s child, yourself in certain situations, or another eligible adult. The type of RESP you choose will depend on your situation, your relationship to the beneficiary, how many children you have, and how much flexibility you want.

In normal parent language: yes, parents can open one. Yes, grandparents can open one. Yes, you can open one even if baby number 2 is still more of a “maybe” than a firm calendar event.

3. What types of RESP plans exist?

There are 3 main types of RESP plans: individual plans, family plans, and group plans. This is where things start sounding like a bank brochure, but stay with me. I promise we are not putting on a grey suit.

Individual RESP

An individual RESP is for one beneficiary. This can make sense if you have one child, if you are opening an RESP for a child who is not related to you, or if you want to keep each child’s education savings completely separate. The upside is that it can be easier to track. The downside is that it may not be as flexible between siblings as a family plan, however it would be possible to transfer the individual RESP to a sibling following certain rules.

Family RESP

A family RESP can be a great option if you have more than one child or plan to have more than one child. You can name more than one beneficiary, and the children generally need to be related to you by blood or adoption. This can include children, stepchildren, grandchildren, adopted grandchildren, brothers, and sisters.

The big advantage is flexibility: if one child needs less money for school and another needs more, a family plan may give you more room to use the RESP money between eligible siblings, as long as the grant rules and lifetime limits are respected.

So if 1 child goes all the way to a PhD and the other decides to become a tech founder in a hoodie at 19, the family plan may give you more flexibility than separate individual plans.

Group RESP plans (hint: you might want to avoid)

Then there are group RESPs, also sometimes oddly called “scholarship plans”. These are the ones I personally side eye. In a group plan, your money is pooled with money from other families whose children are generally the same age. Typically, if you miss a payment, you are kicked out of the “group” and the leftover money is given to the other participants. These plans can be marketed as a responsible education savings option, but they usually have restrictive monthly contribution schedules, carry exorbitant upfront fee structures reaching thousands of dollars, and feature harsh penalties.

I will mention that class actions have been authorized & settled against group plan providers and that you can easily do a google search to find news articles that depict far from positive experiences. There are also reports of predatory-like sales tactics - such as giving a sales pitch to someone who just birthed a baby in a hospital. On top of all of this, Hospital employees have literally pleaded guilty to taking confidential maternity ward records and selling it to RESP Group plan companies so they could market it to new parents.

These sales tactics are a huge reg flag.

Personally, group plans are not Hot Money Mom approved. We are smarter than this.

4. What grants can you get?

This is the fun part: free money.

Canada Education Savings Grant

The main federal grant is the Canada Education Savings Grant, or CESG. The basic CESG gives 20% on the first $2,500 contributed to an RESP each year, up to $500 per year. The lifetime maximum CESG is $7,200 per eligible beneficiary, and lower or middle income families may qualify for additional CESG amounts.

So, in regular human language, if you contribute $2,500 in 1 year, the federal government will add $500. That is before your investments do anything. We love a government top up moment.

If you are behind, you can catch up retroactively one year at a time.

Quebec Education Savings Incentive

In Quebec, we also have the Quebec Education Savings Incentive, or QESI. The basic QESI is 10% of annual RESP contributions, up to $250 per year, and the lifetime maximum is $3,600 per child. Lower income families may also qualify for an additional amount.

So in Quebec, a $2,500 contribution may unlock $500 from the federal government and $250 from Quebec. That is $750 in government money before the market has lifted a single manicured finger - basically a 30% boost just for putting the money in the right account. Not too shabby.

To help low-income and middle-income families, an amount of up to $50 per year, calculated on the basis of family income, may be added to the basic amount.

Just make sure your RESP provider honours the QESI grant: find a list here.

British Columbia Training and Education Savings Grant

Lastly, for our west coast readers, there is also the British Columbia Training and Education Savings Grant. This grant offers a one-time amount of $1,200 to eligible children. The child must be born in 2006 or later and you must apply between the child’s 6th and 9th birthday.

Usually, the institution where you open your RESP (also called the “promoter”) will apply for the government grants automatically on your behalf.

You can add money to the RESP for up to 31 years from the day it was opened, and have up to 35 years to use the money.

The lifetime amount you can contribute of your own money to an RESP is $50,000 perchild. Overcontributing can lead to serious penalties.

5. What about the Canada Learning Bond?

Lower income families may also qualify for the Canada Learning Bond, or “CLB”. This is extra money from the federal government for eligible children, and families do not need to contribute to the RESP to receive it.

Eligible children can receive up to $2,000 through the CLB, including an initial $500 and additional payments of $100 per year until age 15. For the July 1, 2025 to June 30, 2026 benefit year, the income threshold for families with 1 to 3 children is $57,375 or less.

In other words, with the CLB, eligible families can receive money even without making contributions. Enrollment is automatic - just make sure you open an RESP account.

6. How much should you contribute?

Now we are getting into the juicy stuff.

To maximize the basic annual federal grant, you need to generally contribute $2,500 per year per child until you reach a total fof $36,000.

That works out to about $208 per month, or $104 off of a bi-weekly paycheck.

If you are unable to contribute that amount, you can still put less and benefit from the grants. Something is better than nothing.

If you do this for about 14 years, and then contribute $1,000 in the 15th year, you can maximize the basic federal CESG of $7,200. In Quebec, those same contributions may also trigger the QESI for a lifetime maximum of $3,600 per child.

Before investment growth, this already builds a strong education fund of $46,800. But the real magic happens when the money is actually invested and given time to grow.

For example, if someone contributed regularly, received the federal and Quebec grants, and invested the money over many years, the account could potentially grow far beyond the amount personally contributed (keep reading to earn about my investment strategy). Of course, returns are not guaranteed, and your final number will depend on your contributions, grants, investment choices, fees, and market returns.

But the lesson is simple: the earlier you start, the more time the money has to grow. Tiny baby, big timeline.

STARTING LATE OR NOT MAXING OUT THE RESP?

Take a breath: You did not ruin your child’s future.

If you did not open the RESP at birth or could not contribute the full amount every year, you are still able to catch up on missed federal grants.

You can generally only catch up 1 missed grant year at a time. In practical terms, this means that instead of contributing $2,500 in a year, you may contribute up to $5,000 and receive up to $1,000 in CESG that year (the current year grant plus 1 catch up year).

Translation: starting early is great… but starting later is still MUCH better than never starting at all.

7. Should you front load an RESP?

Some people use a strategy called front loading. This means contributing more money earlier in the child’s life so it has more time to grow.

For example, instead of only contributing $2,500 per year, some families may contribute a larger amount in the first year, such as $16,500 and then continue contributing enough each year to maximize grants and the lifetime limit of $50,000 per child. This is very much a “we have extra money lying around” strategy, which is not everyone’s reality. Very rich aunt energy.

But if your child receives cash gifts from grandparents, birthdays, baptisms, baby showers, or relatives who do not know what to buy because your child already has 9 stuffed giraffes, the RESP can be a great place to put that money.

And if contributing $208 per month per child feels like a lot, because it is a lot, you can also ask family members to contribute to the RESP instead of buying more toys. This may be appreciated more than another plastic musical object with no off button.

8. How is an RESP taxed?

RESP money grows tax deferred while it stays inside the account. That means the investment growth is not taxed every year as it happens.

When money is withdrawn for education, there are generally 2 buckets.

The 1st bucket is your original contributions: These are called Post Secondary Education payments, or PSE payments. Since you contributed this money with after tax dollars, it can be withdrawn tax free.

The 2nd bucket is everything else: government grants, bonds, and investment growth. These are called Educational Assistance Payments, or EAPs. EAPs are taxable to the student when withdrawn.

When RESP funds are withdrawn for the benefit of the child, the taxable portion is taxed at the child’s tax rate rather than the parent’s. Since students usually have lower incomes, this often results in little to no tax owing.

This is one of the benefits of the RESP. Students often have lower income and may have tuition credits, so the tax bill may be much lower than if the investment growth were taxed in the parent’s hands.

In other words, the RESP lets the money grow tax deferred, and then the taxable portion is usually taxed in the hands of the broke student. Finally, their lack of income is useful for something.

9. RESP withdrawals

Once your child starts eligible post secondary studies, you can begin withdrawing money from the RESP. However, special rules apply to Educational Assistance Payments (EAPs), which include the government grants and investment growth earned inside the account.

During the first 13 consecutive weeks of studies, EAP withdrawals are generally limited to:

$8,000 for full time students

$4,000 for part time students

After the initial 13 week period, more money can be withdrawn, as long as the student remains eligible. However, there is an annual EAP threshold. For 2026, that threshold is $29,459 (find annual thresholds here). Withdrawals above that amount are still possible, but the RESP provider may need to review whether the amount requested is reasonable based on education related expenses and may ask for supporting documents.

It is also worth noting that these limits apply to EAP withdrawals only (government grants and investment growth). Your original RESP contributions follow different withdrawal rules and are generally not subject to these EAP limits, and thus can be withdrawn beyond the annual threshold limit.

10. What can RESP money be used for ?

RESP money is not just for tuition.

This is one of the biggest myths. The money can be used for eligible education expenses like tuition, rent, books, tools, transportation, and other school related costs (click here for a full list of eligible expenses). The student must be enrolled in an eligible program, but the money is not limited to writing a cheque directly to a university.

Also, the money is not limited to university education. College, cégep, trade school, vocational school, apprenticeship programs, and eligible studies outside Canada also qualify.

RESP MYTH BUSTER

“My child wants to study abroad… guess the RESP is useless?” False.

RESP funds can generally still be used for studies outside Canada, provided the school and program meet the eligibility requirements.

So let them chase their dreams at Berkeley or in the Bahamas… we support options (and letting them do their own laundry).

11. What happens if your child does not go to school?

This is the question that stresses people out.

The good news is that you do not lose everything if your child does not go to post secondary school.

Your original contributions can generally be withdrawn tax free. But Government grants usually have to be returned if they are not used for eligible education. The investment growth may be withdrawn as an Accumulated Income Payment (also called an “AIP”) but taxes and additional penalties up to 20% can apply.

In some cases, you may be able to transfer up to $50,000 of RESP investment growth to your RRSP or spousal RRSP if you have enough contribution room and the conditions are met. Common conditions include that the RESP has been open for at least 10 years and that the beneficiaries are at least 21 and not currently pursuing post secondary education.

Also, your child does not need to go to school immediately after high school. Remember: RESPs can stay open for up to 35 years. So if your child takes a gap year, works for a while, or goes to Europe and comes back with linen pants and a new personality, you may still have options.

12. Can RESP money be transferred to another child?

In some cases, RESP money can be transferred to another RESP, including to a sibling. This can be helpful if one child does not go to school and another child does.

That said, grant limits still apply. For example, if a child has already received the lifetime maximum CESG, excess grants may need to be returned. This is why family RESPs can be attractive for families with multiple children, but also why you need to track the grants by child.

In other words, the government will give you money, but it will not let you freestyle forever.

13. Where should you open an RESP?

In RESP language, the place where you open the account is called the “promoter”. Very fancy. This usually means a bank, financial institution, self directed investing platform, or group plan provider.

I personally prefer self directed investing because I like low-cost ETFs, and I do not want high fees eating my children’s future education money as fast as a toddler eats berries.

Platforms like Wealthsimple (use this referral link for a free $25 when you open an account) and Questrade can be options for self directed investors, but the key is to make sure the provider supports the grants you are eligible for, especially if you live in Quebec and want the QESI.

Wealthsimple’s RESP information currently lists CESG, Additional CESG, CLB, BCTESG, and QESI among the grants available through its RESP offering.

If self-directed investing is not your thing, there is no shame in using an advisor. Just ask about the fees, the investment options, and what happens if your child does not go to school.

You do not need to do everything yourself if you do not want to, but the point is to understand what you are signing.

And if you still opt for a group plan… I cannot say I did not warn you.

14. What should you invest in inside an RESP?

Your RESP can usually hold different types of investments, depending on the promoter. This may include ETFs, mutual funds, GICs, cash, stocks, and bonds.

Personally, I am a big fan of low cost, diversified ETFs. Not because they are exciting: they are not. They are the beige cardigan of investing, and sometimes the beige cardigan is exactly what we need to keep us cozy and warm.

The key is to invest based on your timeline and risk tolerance. If your child is a baby, you may have a long time before the money is needed. If your child is 16, the timeline is much shorter, and you probably do not want the entire account invested aggressively.

As a rule of thumb: the shorter the timeline, the more you want to reduce risk.

How I invest my children’s RESP (not investment advice)

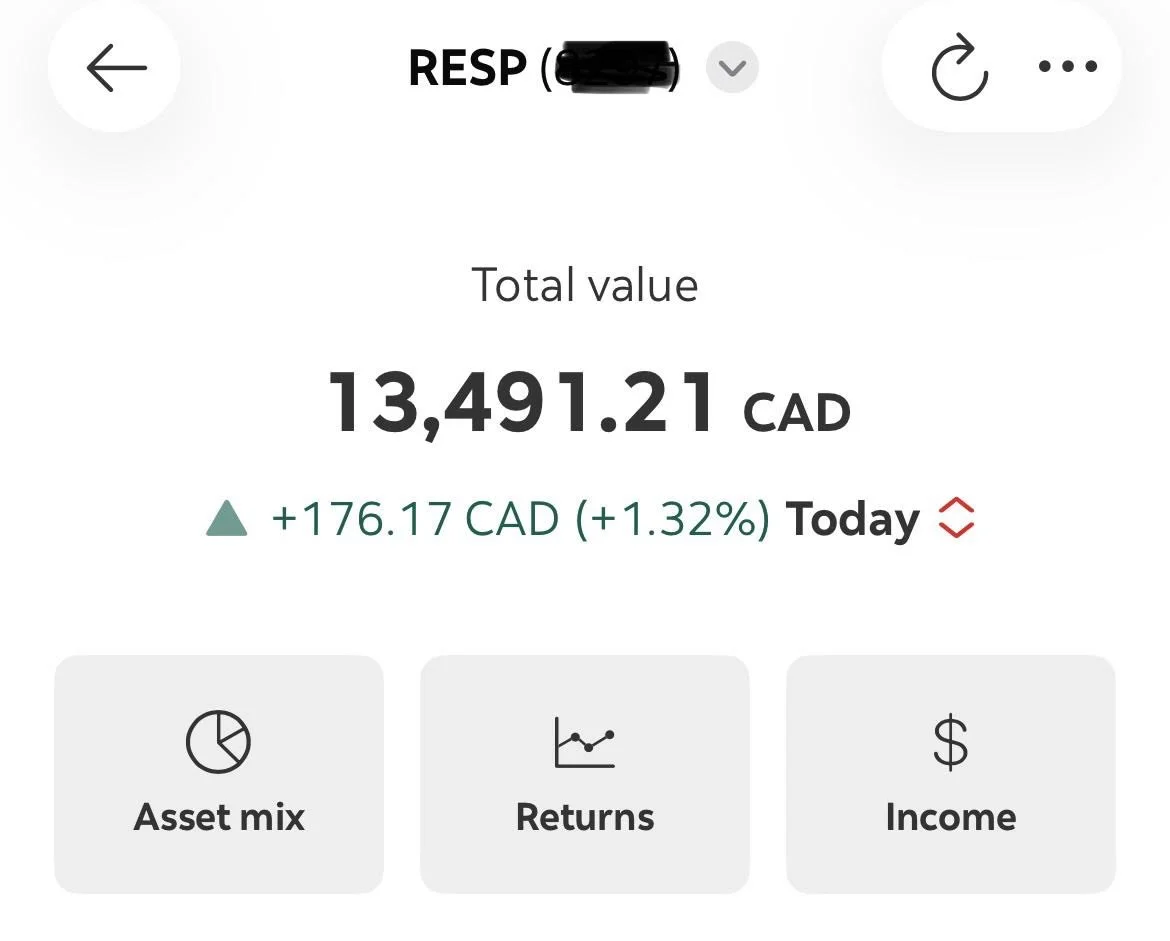

My children are currently 11 months old and almost 3 years old. At the time of writing this, our family RESP, which we opened in 2024, is worth close to $13,500 after we personally contributed $7,700.

We currently invest it in VEQT, a highly diversified all equity ETF, because our kids are still very young and we have time on our side to aim for long term growth.

If you contribute $2,500 per year and receive $750 in government grants annually (if you are in Quebec), assuming 8% annual growth, your child’s RESP could grow to approximately $94,540 after 14 years.

Then imagine making no additional contributions and letting it grow for another 4 years at 4%… and the balance could reach just over $110,000 per child by year 18 after contributing $36,000 of your own money.

That said, we do not plan to keep the RESP this aggressive forever. As our children get closer to higher education, we expect to gradually shift toward lower risk investments to reduce the impact of market volatility.

One possible approach we may consider is:

VEQT while they are very young (a globally diversified 100% equity ETF)

VGRO around age 10 (approximately 80% equity / 20% fixed income)

VBAL around age 14 (approximately 60% equity / 40% fixed income)

Around age 16 to 18, gradually transition part of the portfolio into lower volatility options such as high interest savings ETFs, GICs, cash equivalents or a more conservative allocation

The idea is simple: the closer the money is to being needed, the less risk we may want to take. You mayb also want to be less risky from the start if that is your tolerance (take this quiz to help determine your risk tolerance).

In other words, the shorter the timeline, the more you want to reduce risk in case a full 2008 style market crash right when your fully grown Einsteins need the money for university, cégep, trade school, rent, books, or whatever expensive life path they choose.

15. The takeaway

RESPs can look complicated, but the strategy does not have to be. Here are the key points:

-Open the account early

-Get the grants

-Avoid restrictive group plans

-Keep fees low as much as possible

- Invest according to your timeline

-Reduce risk as your child gets older

And remember that an RESP is not just about university: it can help with many different types of education after high school.

The goal is to give your children more options and less financial stress when they step into adulthood.

Because honestly, they will already have enough to deal with. Rent. Groceries. Tuition. Possibly a weird situationship. The least we can do is try to give them a financial head start.

If you want more (slightly less entertaining than mine) information on the RESP, you can refer to the Government of Canada website.

Laslty, more money content without the finance bro energy, join my newsletter for practical money tips, investing guides and the occasional Hot Money Mom opinion.