The Hot Money Mom Playbook: What To Do When the Stock Market Plummets

The biggest threat to your returns isn’t the market… it’s how you react to it.

In this article, we’ll walk through what to do when the market drops, including how to:

Do nothing (yes, seriously)

Close your app and stop checking

Understand why markets are driven by emotion

Zoom out and stay focused on the long term

Keep an emergency fund so you don’t panic sell

Invest in a way that actually fits your risk tolerance

In 2022, my portfolio was down for almost the entire year.

What did I do?

I kept adding to my investments on schedule… and I didn’t look at my portfolio.

Quite honestly, this wasn’t even a strategy (yet). I was too busy working my butt off and girl bossing in other areas of my life to follow the stock market.

For context, in 2022 the S&P 500, composed of the 500 largest publicly traded U.S. companies, was down a whopping 19.44%.

Oddly enough, that willful blindness worked in my favour.

Adding during downturns is exactly what made my portfolio stronger today. Waiting for things to “feel better” or trying to time the market, meaning guessing when it would hit the bottom or the top, would likely have done more harm than good.

Then the market recovered.

2023 returned 24%.

And 2024 ? It returned 23%.

That’s when something clicked for me, and it had nothing to do with complex strategies or market predictions.

Staying in the game and investing on schedule matters far more than keeping up with the news or trying to time when you put your money into the market.

Investing is a long term strategy: tt is not a get rich quick scheme.

Fast forward to April 7, 2025.

The S&P 500 took a sharp turn and was down 23% from its recent all time high in February.

It was scary, and this uncertainty even had financial institutions scrambling.

So what did I do?

On April 8, 2025, I shrugged and added more money to my already diversified portfolio. A lot more.

The market didn’t just recover, it did so quickly. The S&P 500 returned about 16% from January 2025 to January 2026, and roughly 30% since that April dip. In other words, the money I invested during that drop saw strong returns in a relatively short period.

There are plenty of examples like this: crashes, dips, and blips can happen at any time, whether due to elections, war, COVID-19, or even a tweet by Elon Musk (for real).

For long term investors, they rarely matter.

No one knows exactly what will happen next. What we do know is this: for over more than 100 years, the S&P 500 has returned roughly 10% to 11% per year on average.

That’s the part most people forget when all they see is red on their screens.

So here is your playbook, to stay focused for when the market (and probably everything else) feels like it’s falling apart.

1. Do nothing. Seriously.

The average investor would have better investment results by doing nothing. Here is why: humans aren’t spreadsheets and it is only humans who have bad habits that make us want to buy a stock when it’s “hot” (meaning it probably already reached a high) and panic sell when they are low.

Nothing proves this more by looking at how “Dead” investors outperform the living. Nothing illustrates this better than a well-known Fidelity study, which found that some of the best-performing accounts were the ones left untouched, often because the investor didn’t interfere at all.

The best returns often came from people who didn’t touch their portfolios at all. These were mostly from people who died, or forgotten that they had accounts.

The real flex? Consistency.

No panic selling, no market timing, just steady growth over time.

In other words: be a turtle and not a hare, because doing less actually means more.

So stick to your own investing schedule, as planned. Slow and stedy wins the race.

2. Close your app

This may be the simplest and most underrated strategy: constantly checking your portfolio does not improve performance. It increases the likelihood of reacting emotionally – because the biggest threat to investors is not the market, but their human emotions.

Personally, I keep my banking and my investments in different institutions, so I don’t happen to stumble onto my investment portfolio when doing everyday banking.

Continue investing if that aligns with your plan, then step away. And scroll up to read step one again.

3. The market… she’s a moody b*tch

If the market were on the crazy/hot scale, she would be at the top.

She overreacts to everything, and fluctuations are part of the game.

The part that often forgotten is that markets are driven by sentiment, not just logic.

A company can perform well and still see its stock decline if expectations shift or confidence drops.

The irony is hard to ignore: the market gets called emotional… yet it’s largely driven by institutions and decision makers that are still heavily male dominated.

But yes, tell me more about how women don’t understand money.

4. Zoom out.

Short term, markets feel chaotic. But by looking at the long-term horizon, the picture changes.

Historically, markets have always recovered, but trended upwards over time. Not in a straight line, and not without volatility, but consistently over time, the line goes up.

Looking at a long-term chart of the S&P 500 puts things into perspective. Even major events like the 2008 crash begin to look smaller over time.

Zooming out doesn’t eliminate the volatility, but it makes it easier to understand.

5. Keep an emergency fund

This part isn’t sexy, but this post isn’t about getting a Ferrari by next Wednesday. It’s about building long-term wealth.

An emergency fund exists so you are not forced to withdraw investments at the worst possible time.

Market downturns and unexpected expenses have a way of showing up together.

Keeping cash in a liquid, accessible account, such as a high interest savings account, provides that buffer.

Most recommendations suggest holding 3 to 6 months of expenses, with some preferring closer to 12 months for additional security.

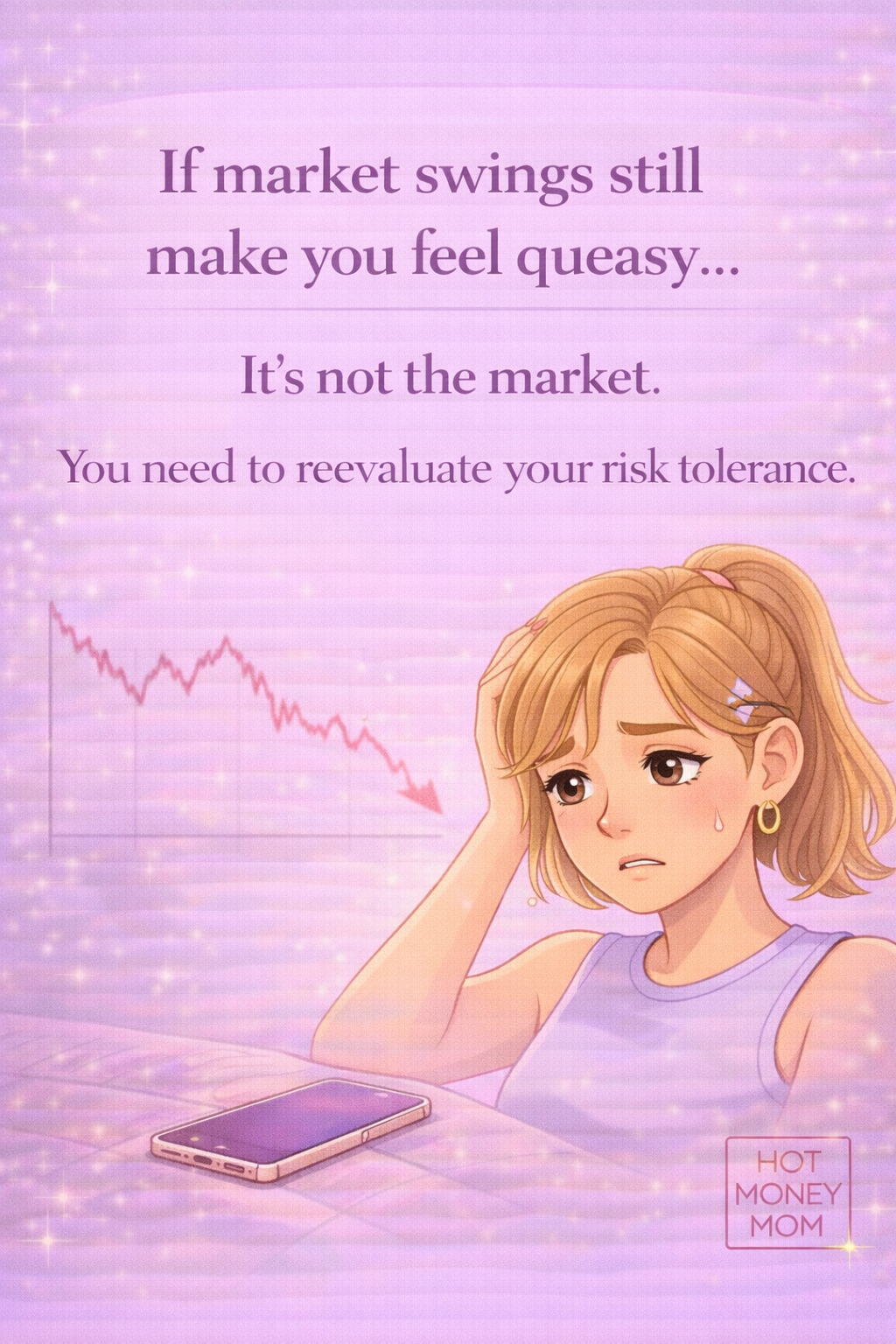

6. Understand your own risk tolerance

If steps 1 through 6 aren’t working, that is OK – no one is shaming you here and investing isn’t one size fits all. It’s more like skincare, you need to find what actually works for your skin type.

Market downturns often reveal your true risk tolerance more clearly than any questionnaire ever could.

We work hard for our money, and watching it drop is not for the faint of heart.

This part we forget: it is easy to feel comfortable with risk when markets are rising, but when things take a turn you might need to reassess what your risk tolerance actually is.

There are plenty of options designed for different risk levels, and there is no prize for stressing yourself out.

So maybe it’s time to reassess, step back from DIY investing if needed, speak to an advisor, and consider adding safer options like bonds or GICs into the mix.

The takeaway

The market will not move in a straight line.

There will be red days, dips, and corrections. The experience can feel like a wild ride, especially when emotions get involved.

For long term investors, these movements are part of the process.

Historically, markets trend upward over time.

Turn off the noise, take a sip of your latte, and keep investing on schedule. You might just be buying at a discount… and in the stock market, the best deals rarely feel good in the moment.

Read Step 1 again. If that is still too much for you, reassess your investment plan.