Part 3: How to Save for your First Home Without Losing Your Personality - (Free Checklist Included)

A smart, realistic guide to building your down payment in Canada using your FHSA, RRSP, TFSA and strategic assistance programs - with real numbers

This article will cover a 5 Step Strategy to Save for a Down Payment in Canada:

Use the right accounts (FHSA, RRSP, TFSA)

Check federal, provincial and municipal assistance programs

Invest your savings according to your timeline

Build an automated saving system

Understand the real numbers for your down payment

Saving for a home can feel overwhelming, and it might even feel unrealistic. Maybe you came into some money, maybe you have a five year plan color coded in your notebook, or maybe you are mentally preparing to live off ramen, thrifted blazers, and four roommates in order to make this dream happen. Funny not funny.

But here is the truth: you can make dreams a reality.

With a plan and a little discipline, homeownership can move from “one day” to “in progress.” And who knows? Sometimes life cooperates: a salary bump, a bonus, a generous gift from someone who loves you. If that happens, that is not upgrade your handbag money, this should be used as upgrade your life money.

According to CMHC’s 2025 Mortgage Consumer Survey, Canadian homebuyers saved for about 3.4 years on average for their down payment. So no, it is not instant. But it is doable.

This is not a post about whether you should buy a home (Click here for a Rent v. Buy calculator): this is about how to save for one efficiently because there is a smart way to do this. And we like doing things the smart way.

Now, let’s talk strategy.

1. Start With the Right Accounts

If you are serious about buying a home, you do not just “save”. You need to optimize how do it.

The following 3 registered accounts can make a big difference when used wisely:

Can you combine FHSA and the Home Buyers Plan?

Yes. Buyers can withdraw from both, which can significantly increase the amount available for a down payment.

The First Home Savings Account (FHSA), introduced in 2023, is one of the most powerful tools available. You can contribute up to $8,000 per year, up to a lifetime maximum of $40,000 dollars per person. The total timeline to do this is 15 years. Contributions are tax deductible, growth is tax free, and withdrawals for a qualifying first home are tax free. And unlike the RRSP Home Buyers’ Plan, there is no repayment required. If you don’t end up buying a home, you can roll it into your RRSP. It is essentially the overachiever of registered accounts. Click here for more details on the FHSA.

Next is the RRSP through the Home Buyers’ Plan. This allows you to withdraw up to $60 000 from your RRSP for your first home, but you must repay it over 15 years. It can be a useful tool, especially because RRSP contributions reduce your taxable income. Just remember: you are borrowing from your retirement, not creating free money. If you are disabled, the first time buyer requirement is waved. Click here to verify your eligibility for the RRSP Home Buyer’s Plan and here for more on RRSP accounts.

And then there is the Tax Free Savings Account (TFSA). No deduction going in, but completely tax free growth and flexible withdrawals. If your FHSA is maxed and you want flexibility, the TFSA is an excellent place to build your down payment fund. Click here for more details on the TFSA.

You can even combine the FHSA and the RRSP Home Buyers’ Plan: if you max out the contributions that will add up to a cool$100,000 down payment, not accounting for interest accumulated in your FHSA.

For couples these amount doubles since each person can withdraw from their own accounts - just make sure you are both eligible. That doubles the potential strategy. Many buyers do not realize this.

For example, if two partners each max out their FHSA, that is $80,000 in contributions alone before investment growth.

These accounts are not small strategy: they are grown woman strategy.

2. Other assistance programs

These might not be utilized enough: before you assume all costs to owning a home are entirely on you, it is worth checking what support already exists. There are federal, provincial, and municipal programs that can lower your upfront costs or reduce your monthly payments.

Many first time buyers never look into them - it’s essentially free money.

Municipal assistance programs

Major cities across Canada periodically offer down payment assistance or shared equity programs for first time buyers. These are usually income tested and may be limited to specific property types or price caps. For example, Montreal offers a Home Purchase Assistance Program through which qualifying buyers can receive either a lump sum when they purchase a new property or a refund of their real estate transfer tax (welcome tax) if you purchase an existing property. These sums vary from $5,000 and can go all the way up to $15,000.

Eligibility depends on income, property type, and location, but these amounts can meaningfully reduce costs associated with buying a home. It is always worth checking your city’s housing department before you buy.

Provincial assistance programs

In addition, many provinces offer land transfer tax rebates/exemptions for first time buyers. In places like Ontario and British Columbia, eligible buyers can reduce or even eliminate the provincial land transfer tax up to certain purchase price thresholds. That can save thousands of dollars on closing day.

Some regions go even further by offering down payment assistance in the form of interest free loans. Cities such as London and provinces like Nova Scotia have offered programs that help buyers bridge the gap on their down payment. The details vary by region and income level, but if you qualify, it can significantly reduce the amount of cash you need upfront.

The First Time Homebuyer’s (FTHB) GST/HST rebate

If you are buying, building, or substantially renovating your first home, there is another program worth knowing about: the FTHBGST/HST New Housing Rebate.

One important detail: this program applies to new homes or major renovations. If you are buying a resale property, GST usually does not apply in the first place.

In simple terms, it allows eligible buyers to recover some or all of the GST paid on a new home.

And since GST is 5% of the purchase price, that can translate into a lot of money.

To qualify, the home must:

be newly built or substantially renovated

be used as your primary residence

Here is how the rebate works:

Homes up to $1 million → buyers may recover up to 100% of the GST, up to a maximum rebate of $50,000

Homes between $1 million and $1.5 million → the rebate is gradually reduced

Homes above $1.5 million → no rebate is available

In other words, if you are buying a new build, this rebate could shave tens of thousands of dollars off your purchase. Read more about it here.

Tax credits

Also, do not forget about Tax Credits. The Federal Home Buyers' Amount is a non refundable tax credit available to eligible first time buyers. It reduces the federal income tax you owe in the year you purchase a qualifying home.

Quebec has it’s own Home Buyer’s tax credit which can be claimed on top of the federal one. If your move is tied to a new job or business and you are relocating at least 40 km closer, you may also be eligible to deduct certain moving expenses under CRA rules.

These will not generate a refund if you have no tax payable, but they are still something to look into.

The Takeaway

The bottom line is simple: before you assume you are on your own, check what is available in your city, your province, and at the federal level. These programs can reduce the pressure on your savings and make your path to home ownership more manageable.

In other words: taking the time to do reserach and read the fine print just might pay off.

3.. How to Invest While You Save

This is the part people rarely explain clearly, and this is where people can easily mess up. You need to invest from the registered accounts mentioned above. I have to repeat this: this means stashing the money in your FHSA/RRSP/TFSA won’t work the magic on it’s own: you need to buy an investment product like stocks, bonds, ETFs or mutual funds, from within these accounts. Look at the accounts as the pots you grow flowers in - the flowers being your investments.

How you invest depends on your timeline & risk tolerance.

As a rule of thumb, something like this works well for many people (this is not investment advice: please see the discalimer at the bottom of the page, do your own research and speak with a professional).:

If homeownership is 10 years or more away, you can afford to be more growth focused. A higher equity allocation (meaning more money in stocks) may make sense because you have time to ride out market swings. A highly diversified full equity ETF like XEQT might fit the bill (Fun tidbit: this ETF is so popular it has it’s own subreddit called r/justbuyXEQT). If full equity isn’t for you, you might want to start with something like VGRO (80/20 equity/bond split).

If you are 4 to 6 years out from homeownership, a balanced approach, often a mix of equities and bonds, can help you grow your money while managing risk. An ETF like VBAL might be for you (60/40 equity/bond split).

If you are within a few years of buying, preservation becomes the priority. At that stage, you may want to move toward conservative options such as GICs, high interest savings products, or ultra conservative ETFs. If the market decides to have a mood swing the year you need your down payment, your money will be secure. We do not want to relive 2008 drama right when you need cash for a down payment.

The lesson here is: as your timeline shortens, your risk should decrease. Certainty is better when a notary appointment is on your calendar.

4. Build a Saving System, Not Just a Wish

Dreams are cute, but systems build down payments.

If buying a home is the goal, your budget needs to reflect it. That means deciding, in advance, how much of your income is going toward that down payment. 5% ? 10% ? Or maybe even 20% during your high income era (or while still living with 4 roommates ).

When you start diving into financial education you will hear this saying over and over again: “pay yourself first”. This means automate your savings so the money leaves your account before you have time to spend it on things that sparkle.

Windfalls should also have a job. Tax refund? Bonus? Unexpected cash? That is not vacation money, see it as down payment acceleration.

Be consistent with your savings: it will beat intensity every time.

5. Now, let’s Talk Numbers

I saved this part for later on purpose because this is where people usually click away. But stay with me. We are about to crunch real numbers, just like your high school math teacher promised you would one day.

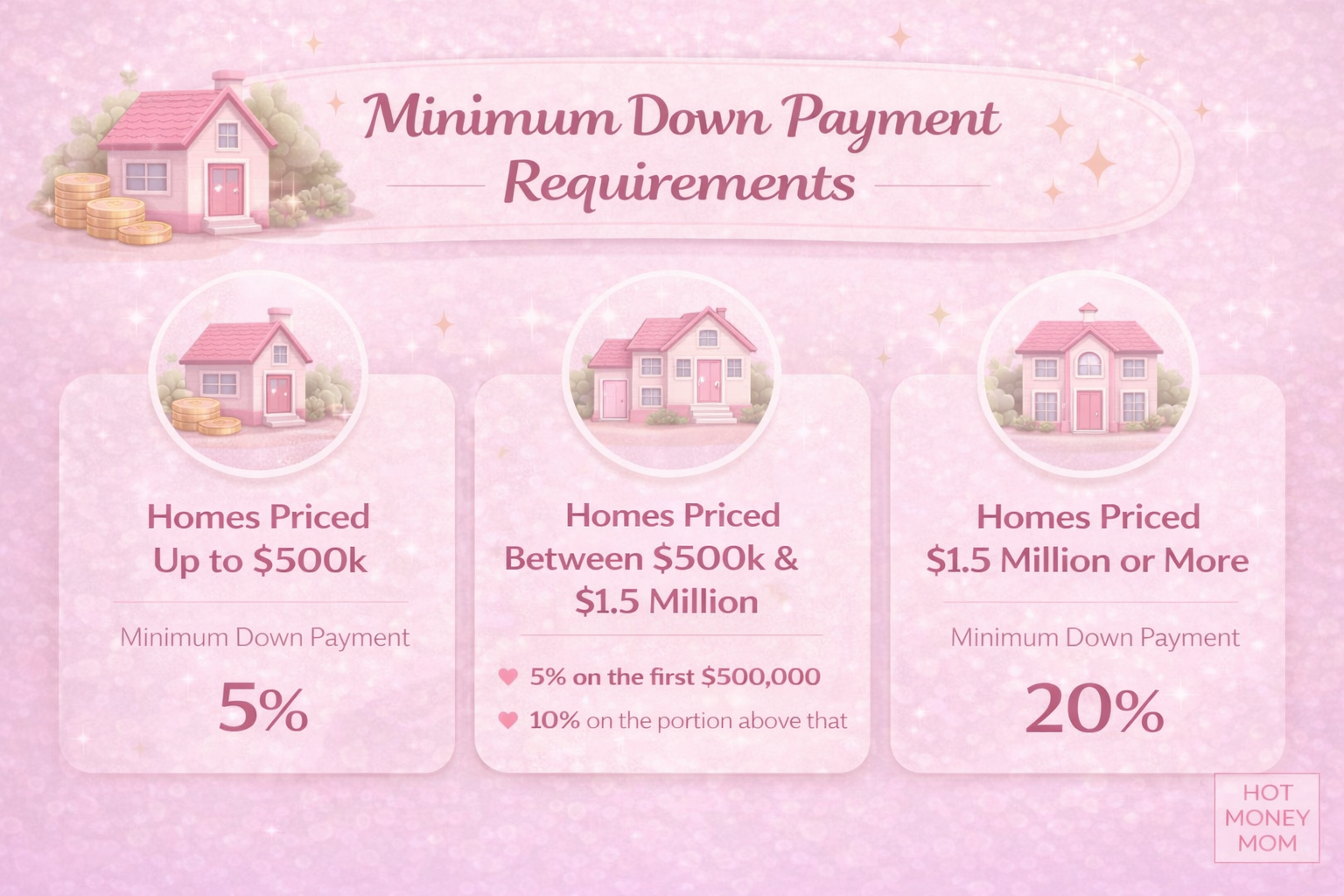

In Canada, the minimum down payment depends on the purchase price of the home:

5% for homes priced $500,000 or less:

So on a $500,000 home, you need a minimum of$25,000

For homes priced more than $500,000, but less than $1,500,000:

You will need to add two amounts. The first is 5% of $500,000. The second amount is 10% of the remaining price of the home.Ex. on a $750,000 home:

$500,000 x 5% = $25,000

$250,000 x 10% = $25,000

$25,000 + $25,000 = $50,000 minimum down payment

For homes priced $1,500,000 and over, you need to multiply by 20%:

Ex. on a $1,500,000 home:

$1,500,000 x 20% = $300,000 minimum down payment

That is the floor, not the ceiling.

A larger down payment can reduce your monthly payment, lower the total interest you pay, and potentially help you avoid mortgage default insurance. When your down payment is less than 20%, mortgage default insurance is required. Read more about it here.

To calculate how much your mortgage payments could cost, you can refer this calculator.

Also, we cannot forget to mention closing costs. In Canada, these typically range from about 1.5% to 4% of the purchase price. On a $500 000 home, that could mean roughly $7,500 to $20,000 for land transfer tax (or the “Welcome tax” in Quebec), legal fees, inspections, and adjustments.

I know what you are thinking: Ouch. But knowing early prevents unwanted surprises later.

These numbers can sound intense at first, but let’s break it down.

As of early 2026, the national average home price in Canada was about $652,941.At that price, the minimum down payment would be approximately $41,000.

That is essentially 5 years of maxing out your FHSA at $8,000 per year, bringing you to $40,000 in contributions alone.

Broken down further, that is about $666 per month or roughly $333 bi weekly.

If you are buying with a partner, that is roughly $167 eachthat you each need to stash away bi-weekly to meet the goal.

Framed that way, it becomes a structured savings plan rather than an overwhelming lump sum.

And remember, FHSA contributions reduce your taxable income, which can generate a tax refund that you can reinvest to move even faster. This also does not factor in any investment growth earned inside the FHSA over those 5 years. The number does not shrink,: instead your strategy grows.

Final Takeway

Ramen noodle jokes aside, saving for a home doesn’t have to be about deprivation, it is about planning ahead.

No one said it was going to be easy.

But by using the right accounts, investing according to your timeline, automating your savings & understanding the numbers, you can make it happen. Adjust as you go.

It may take a few years, but that is normal: it’s only the biggest purchase of your life.

But if you build a plan and stick to it, that dream backyard, that walk-in closet, that “forever” or “for now” place becomes much more than a Pinterest board.

And your Hot Money Mom fully believes you can make it happen. Use the links and calculators on my Resources page to help start your journey and click below to download your free printable checklist:

Don’t forget to subscribe to my newsletter to never miss a checklist.