Part 1: What Is a Mortgage and How Does It Work?

Understanding your mortgage is not boring: it is powerful.

So you have been contributing to your FHSA and you beat the odds, or you are at least trying to, and managed to save for a down payment and start looking for a home you love. Congratulations: that alone deserves a moment.

But now comes the most adult thing an adult can do, right after having children, and that is securing a mortgage.

This is not an article about whether or not you should buy a home (Click here for a Rent v. Buy calculator). This is about how a mortgage works so you actually understand what you are getting into.

Let’s demystify it.

What a Mortgage is in clear terms

At its core, a mortgage is a loan you take from a lender, usually a bank, to buy a property. You use the bank’s money to pay the seller, and then you slowly pay the bank back over time with interest.

That loan is legally tied to your home and registered with your provincial land registry. This means if you stop making payments and default, the bank can take the house through foreclosure. We are not aiming for that storyline.

The down payment

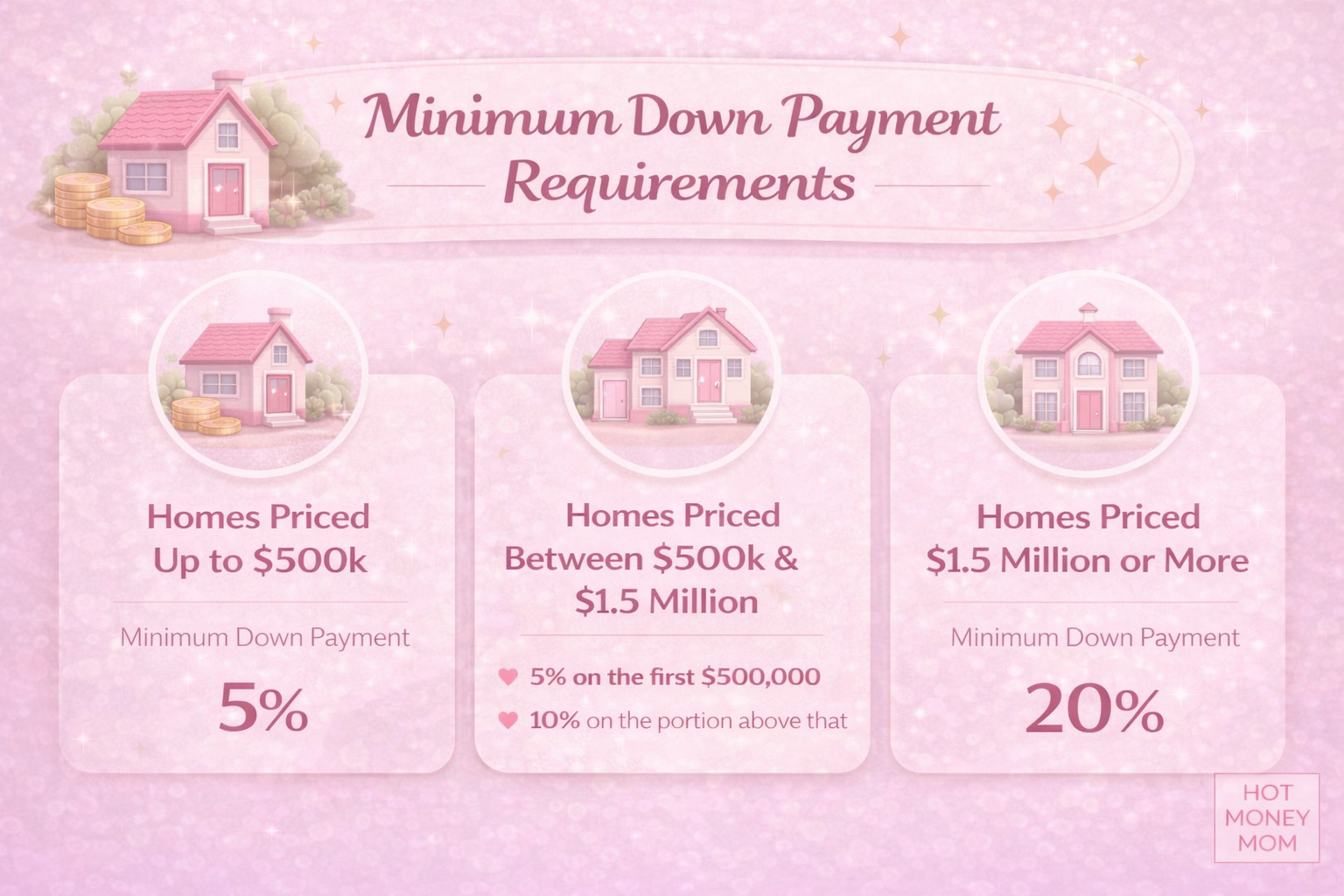

In Canada, the minimum down payment depends on the purchase price of the home.

For homes priced up to $500,000, the minimum down payment is 5%. For homes between $500,000 and $1.5 million, it is 5% on the first $500,000 and 10% on the portion above that. For homes priced at $1.5 million or more, you need at least 20%.

These are the minimum requirements, if you put down less than 20%, you will have to get mortgage default insurance, which we will tackle in the next part.

Mortgage default insurance

If your down payment is less than 20%, you are required to take out mortgage default insurance. This is often misunderstood, so let’s clear it up.

Mortgage default insurance protects the lender, not you. It allows the bank to lend to buyers with smaller down payments by insuring the loan in case of default. If you stop making payments and the home is sold at a loss, the insurer covers the shortfall for the bank. You still lose the home and can still be pursued for any remaining balance.

If that feels unfair, here is an analogy that helps. Mortgage default insurance is like insurance on a rental car. It protects the company that owns the car, not the person driving it (even though you do own your home…).

The premium is calculated as a percentage of the amount you borrow. The smaller your down payment, the higher the premium. It can usually be added to your mortgage balance and paid over time, which means interest applies to it as well.

That said, the interest rate you obtain on your mortgage can be lower when you have this insurance, but it is usually not enough to offset the cost.

Amortization versus term

These two words get mixed up constantly and they are not the same thing.

The mortgage term is the length of time you commit to a specific rate, lender, and set of conditions. Common terms are 3 or 5 years. When the term ends, you renew your mortgage on the remaining balance at whatever rates are available at that time.

The amortization period is the total length of time it will take to fully pay off your mortgage. In Canada, the typical maximum amortization is 25 years, though some borrowers qualify for longer, up to a maximum of 30 years.

Think of amortization as the full marathon. The term is just the pair of shoes you are wearing right now. You will change shoes several times before the race is over.

Longer amortizations mean lower payments but more interest over time. Shorter amortizations mean higher payments but less interest paid overall.

Fixed versus variable

A fixed rate mortgage means your rate and payment stay the same for the entire term. It offers predictability and stability, but you miss out if rates drop.

A variable rate mortgage moves with the market. Your rate fluctuates based on changes to the prime rate. This can save you money when rates fall and often comes with lower penalties if you break the mortgage early, but it also means payments can increase if rates rise.

A simple way to think about it is booking a flight: fixed is locking in the price months in advance for peace of mind. Variable is waiting to see if prices drop closer to departure; you are taking a risk. Neither is wrong, they just serve different personalities.

Payment frequency and why it’s important

Most people default to monthly payments, but you usually have several options. Paying more frequently means more money goes toward the principal sooner, which reduces interest over time.

Accelerated biweekly payments are especially powerful. They are structured so you make the equivalent of one extra monthly payment per year. This can shave literal years off your mortgage and save tens of thousands in interest.

It is one of the simplest moves homeowners can make to pay off that mortgage sooner.

Who determines your interest rate

Your mortgage rate does not come out of thin air and it is not just something your bank makes up on a whim: it is influenced by bond yields and the Bank of Canada’s policy rate depending on whether you choose a fixed or a variable mortgage. Let’s break it down.

Fixed mortgage rates mostly follow Government of Canada bond yields, especially the 5 year bond. These are the same bonds investors can buy. A bond is basically a loan to the government that pays interest over a set period. When investors demand higher interest to hold those bonds, bond yields rise and fixed mortgage rates usually rise too. When yields fall, fixed mortgage rates tend to fall as well.

Lenders typically price fixed mortgage rates above bond yields, adding a margin to cover lending risk and costs.

This is why mortgage rates sometimes move even when the Bank of Canada hasn’t done anything yet.

Variable mortgage rates work differently. They are tied directly to the Bank of Canada’s policy interest rate, (also called the “overnight rate”), which influences the banks’ prime rate. When the Bank of Canada raises or cuts its rate, variable mortgages usually move shortly after. The Bank of Canada adjusts this rate 8 times a year to control inflation, stabilize the economy, and keep employment levels healthy.

In other words: fixed rates listen to what the bond market thinks will happen to rates, while variable rates react to what the Bank of Canada actually does.

So your mortgage rate is driven mostly by timing and market conditions, but are also affected by borrower (that’s you!) details like: credit score, down payment amount & loan-to-value ratioe.

And there is a little wiggle room to negotiate around the edges.

The cost of interest

This part hurts a little, and by little I mean a lot. But it is important.

When you make a mortgage payment, it is not a fifty fifty split. Interest is the fee you pay the bank to borrow the money, and principal is what actually goes toward owning your home. In the early years, a much bigger portion goes to interest. The bank gets paid first.

For example, on a $500,000 mortgage at 5% interest with a 25 year amortization, your monthly payment is about $2,908.

Over the first 5 year term, you will make 60 monthly payments totaling about $174,000. Of that amount, more than $117,000 goes to interest and only about $57,000 goes toward the principal. At the end of those 5 years, you still owe roughly $443,000 on your mortgage, despite having made $174,000 in payments. Ouch.

That is not a mistake or a scam. It is just how mortgages are structured. And yes, the bank wins.

Early on, paying down your mortgage can feel like trying to empty a bathtub while the tap is still running. This is why small changes, like accelerated payments or extra lump sums, have an outsized impact. They go after the principal when interest is doing the most damage.

Where to get a mortgage

In Canada, most people get a mortgage either directly from a bank or through a mortgage broker. Both can work, but they are not the same.

The most important thing is not where you get the mortgage, but that you understand the one you sign.

When you go to a bank, you are offered that bank’s products only. It is simple and familiar, especially if you already do your everyday banking there. The tradeoff is that you are not seeing what other lenders might offer.

A mortgage broker does not lend money; instead they do the shopping for you. They search across multiple lenders, including banks and credit unions, to find options that fit your situation. This can be especially helpful for first time buyers or anyone who wants to compare rates and features without doing all the legwork themselves. Brokers do not charge you for this work.

Some people also get their mortgage directly through a credit union. Credit unions are member owned and can sometimes offer more flexibility or competitive terms, especially for local buyers.

There are also private or alternative “B” lenders. These are usually a backup option for people who do not fit traditional bank criteria and typically come with higher rates and shorter terms. This is not where most buyers start, and probably not the best option, but it is part of the landscape.

There is no rule saying you have to choose one path. You can talk to a bank, a broker, and even a credit union, compare offers, and decide what feels right. This is a financial contract, not a loyalty program. As I always say, be loyal to your bank account, not to a corporation.

Can you make extra payments if you come into money ?

Yes. Most mortgages allow prepayments through lump sums or increased regular payments, often capped at 10% or 20% per year. These extra payments go directly toward the principal and reduce both interest and amortization length.

Always check your contract for limits and penalties. And yes, sometimes investing that money instead may make more sense depending on returns and interest rates. That is a whole other post.

The takeaway

You can find daily mortgage rate updates on the Financial Post website and refer to my Resources with an entire section dedicated to everything mortages, including calculators.

For now, just know this: you have more control than you think.

If you are preparing to buy a new home, you might also want to read Part 2: How to Secure the Best Mortgage Rate.

Don’t want to miss other posts like this one ? Subscribe to my newsletter to stay informed.